#This tells python to draw the graphs "inline" - in the notebook

%matplotlib inline

import matplotlib.pyplot as plt

import statsmodels.api as sm

from math import sqrt

from numpy.random import seed

from numpy.random import randn

from numpy import mean

from scipy.stats import sem

import statistics

import seaborn as sns

from IPython.display import display, Math, Latex, display_latex

import plotly.express as px

import pylab

import pandas as pd

import numpy as np

# make the plots (graphs) a little wider by default

pylab.rcParams['figure.figsize'] = (10., 8.)

sns.set(font_scale=1.5)

sns.set_style("white")

Regression

Workshop 7

Aims:

In this workshop, we’re going to be modeling the relationship between education and income. More precisely, we’re going to be looking at the effect of increasing education on hourly wages using Ordinary Least Squares regression. We’re going to accomplish this in four steps:

- Summary Statistics

- Table of Summary Statistics

- Visualisation

- Exploratory Plots

- Assumptions

- A. Independence

- B. Heteroscedasticity: Regression plots + Q-Q plot

- C. Multicollinearity: VIF + Correlation Matrix

- Regression

- Regression Table

If you’re conducting a regression, you must complete the steps above, and produce each item indicated by a bullet point.

Getting Started

As always we’ll start by importing the libraries I need

Now that I’ve imported the libraries I’m going to be using, I’m ready to import the data:

df=pd.read_csv('https://storage.googleapis.com/qm2/wk7/cps.csv')

df.head()| year | state | age | sex | race | sch | ind | union | incwage | realhrwage | occupation | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1990 | 36 | 58 | 1 | 3 | 12.0 | 871 | 0.0 | 14200.0 | 12.269874 | Office and Admin Support |

| 1 | 2009 | 5 | 28 | 1 | 1 | 12.0 | 8660 | 1.0 | 17680.0 | 8.635149 | Office and Admin Support |

| 2 | 1990 | 36 | 37 | 1 | 1 | 14.0 | 380 | 1.0 | 28000.0 | 21.169851 | . |

| 3 | 1990 | 6 | 34 | 1 | 1 | 18.0 | 740 | 1.0 | 27500.0 | 20.447746 | Computer and Math Technicians |

| 4 | 1981 | 51 | 38 | 1 | 4 | 13.0 | 798 | NaN | 17000.0 | 18.892282 | Managers |

Our dataframe has 10 columns:

- year: Survey year

- age: the person’s age

- sex: the person’s sex

- 1=male

- 2=female

- race: the person’s race

- White non hispanic=1

- Black non hispanic=2

- Hispanic=3

- Other non hispanic=4)

- sch: Educational attainment

- None = 0,

- Grades 1-12 = 1-12

- Some University = 13,

- Associate’s degree = 14,

- BA = 16

- Advanced Degree = 18

- union: Union membership

- N/A = 0,

- No union coverage = 1,

- Member of labor union=2,

- Covered by union but not a member=3

- incwage: Wage and salary income

- realhrwage: Real Hourly Wage

- occupation: Occupation

- ind: industry code

- state: FIPS code denoting the state of residence.

We’ll begin, as we did with last week’s workshop, by selecting the year 2013 in our data and making sure that all the variables that represent categories are stored as categorical in python:

reg_df=df[df['year']==2013].drop(['year'],axis=1) # filter the whole dataset to 2013 and drop year column

reg_df[['race','union','sex','occupation','ind','state']]=reg_df[['race','union','sex','occupation', 'ind','state']].astype('category') # convert these columns to categorical1. Summary Statistics

Once our data has been cleaned and all our variables are stored as the appropriate type, we can start with the first step of any regression project: creating a table of summary statistics. This is an important part of the process, since it gives the reader a qualitative understanding of your data before you analyze it. It also serves to demonstrate that you’ve cleaned the data appropriately, and that the measures of the variables make sense.

summary=reg_df.describe().round(2) # generate summary statistics, and round everything to 2 decimal degrees

summary=summary.T #.T transposes the table (rows become columns and vice versa)

summary| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| age | 53790.0 | 42.91 | 10.56 | 25.00 | 34.00 | 43.00 | 51.00 | 64.0 |

| sch | 53790.0 | 13.93 | 2.74 | 0.00 | 12.00 | 13.00 | 16.00 | 18.0 |

| incwage | 53790.0 | 51821.86 | 60163.45 | 38.00 | 24000.00 | 40000.00 | 63000.00 | 1102999.0 |

| realhrwage | 53790.0 | 24.38 | 151.90 | 2.01 | 12.17 | 18.44 | 28.12 | 34760.8 |

This table is already informative. I now know that the average person in this dataset is 42 years old, has around 14 years of schooling, and makes $24/hour (or $51,821/year). However, it’s also useful to spot potential errors in data entry that may warrant greater attention.

Notice the max value for real hourly wage. Despite the fact that those in the top 75% of earners make $28.12/hour, someone is making $34,760 per hour. Must be nice (or, may be a data entry error). Either way, because regresisons are sensitive to this sort of outlier, we should remove it. I’ve defined a function below that calculates the quartiles and filters out observations that are more than three times as far away form the top quartile as the top quartile is from the bottom one. This was a somewhat arbitrary choice, but it allows me to be consistent if I want to apply it to other variables. You could also just pick a cutoff qualitatively and justify it (e.g. “I will focus on those making up to $250k per year, since they represent the population i’m trying to understand”).

def filter_outliers(var):

q1 = var.quantile(0.25) # calculate the first quartile

q3 = var.quantile(0.75) # calculate the third quartile

iqr = q3 - q1 # calculate the interquartile range

low = q1 - 3*iqr # calculate the lower bound

high = q3 + 3*iqr # calculate the upper bound

filtered = reg_df[(var > low) & (var < high)] # filter the values that are within the bounds

dropped_observations= len(var)-len(filtered) # calculate the number of observations that were dropped

print('Dropped {} observations'.format(dropped_observations))

return filtered

reg_df=filter_outliers(reg_df['realhrwage']) # filter outliers from realhrwageDropped 1040 observationsWe can see that this operation dropped 1040 observations that had extreme values in the “realhrwage” variable. Let’s re-generate the table of summary statistics and only keep four columns: count, mean, standard deviaiton, minimum, and maximum.

summary=reg_df.describe().round(2).T

summary[['count','mean','std','min','max']]| count | mean | std | min | max | |

|---|---|---|---|---|---|

| age | 52750.0 | 42.84 | 10.57 | 25.00 | 64.00 |

| sch | 52750.0 | 13.88 | 2.73 | 0.00 | 18.00 |

| incwage | 52750.0 | 46849.39 | 33376.96 | 38.00 | 353000.00 |

| realhrwage | 52750.0 | 21.59 | 13.03 | 2.01 | 75.81 |

2. Visualization

The summary statistics table provides us with a good overview of some of the variables we’re interested in. However, you’ll notice that it omits many of the other variables in our dataset: the categorical ones. This is because calculating the mean, standard deviation, etc. of something like the “occupation” column doesn’t really make sense. For that, we turn to visualization.

Visualizing the distribution of categorical variables

So far in this course we’ve been using a python library called Matplotlib to make our visualizations, which we’ve been calling using the ‘plt’ alias. But this isn’t the only one that is avaialble to us. Seaborn is another library that has some cool plotting functions that are more geared towards statistical analysis. We’ve already imported seaborn above, and we’ll be calling it using the alias “sns”. We can use it in conjunction with matplotlib.

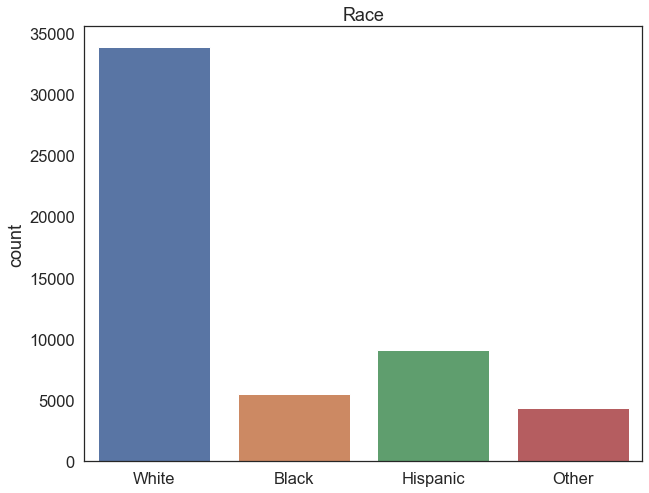

To get a sense of the distribution of our categorical variables, we’ll make some plots that count the number of observations in each category. Let’s start with the race category:

sns.countplot(data=reg_df, x='race') # plot the union variable

plt.title('Race') # add a title

plt.xlabel('') # remove the x axis label

plt.xticks(ticks=[0,1,2,3],labels=['White', 'Black','Hispanic','Other']) # replace the x axis labels with more descriptive labels

plt.show() # show the plot

Exercise

- Generate an equivalent plot for the other categorical columns

- What is the most common industry code, and what does it correpsond to?

3. Assumptions

Once you’ve generated summary statistics for your continuous variables and exploratory plots for the categorical ones, it’s time to start thinking about the relationships between the variables. Today, we’re going to be modeling a linear relationship between income and years of schooling, by means of a linear regression. But before we do that, we need to check a couple things– all statistical tests have a number of assumptions that must be satisfied in order to yield robust results. Before we run a regression, we must check that the assumptions in this case are satisfied. There are four main ones:

A. Indepdendence

B. Homoscedasticity

C. Multicollinearity Let’s go through them one by one.

A. Independence

Linear regression assumes that measurements for each sample subject are in no way influenced by or related to the measurements of other subjects.

Though in the full CPS dataset we have repeat observations of the same individual over time, we’ve only been analyzing one year’s worth of data, so we satisfy the independence assumption. If we ran a regression on the full sample over multiple years, this would violate the independence assumption. It’s very possible to run a regression with repeat observations of the same units (people, places, etc.) over time, but you need to use a special type of regression called a panel regression. More on that next week.

B. Homoscedasticity

Linear regression assumes that the variance of residuals is the same for any value of x, and that residuals are normally distributed with a mean of 0.

This is a complicated way of saying your regression line should fit consistently across the full range of \(x\) values. If there are really small residuals (i.e., all the data points are close to the line) for low values of \(x\), but larger residuals for high values of \(x\), the regression is not performing well– we wouldn’t have the same confidence in our predictions at different values of \(x\). Similarly, if all the residuals are on one side of the regression line in different parts of the \(x\) range, the model will consistently over/underestimate in those regions. When the variance of residuals from a regression model are inconsistent, we have Heteroscedasticity.

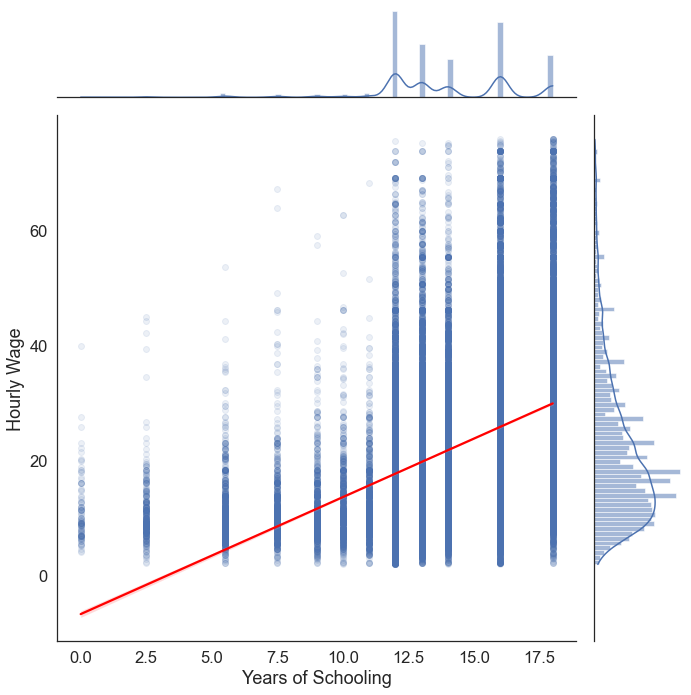

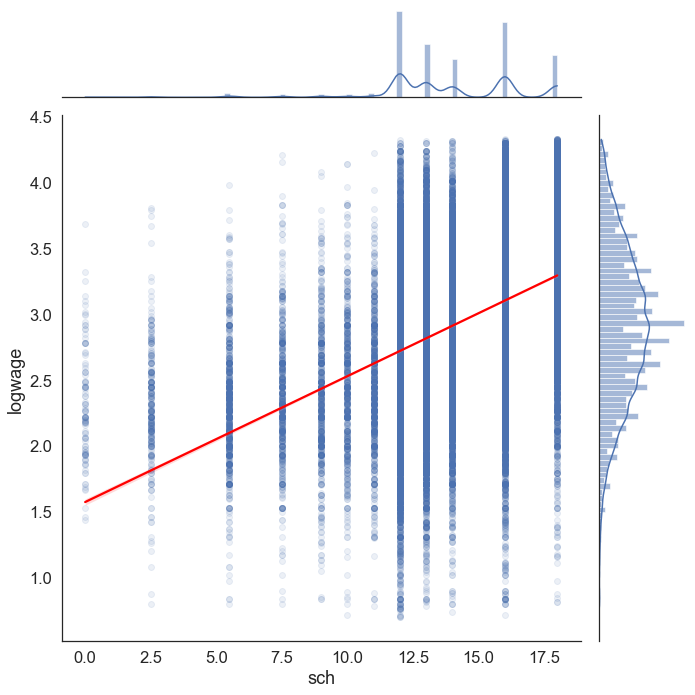

We can explore potential heteroscedasticity by visually inspecting a regression plot. In our case, we’re primarily interested in the relationship between years of schooling and hourly wages, so we’ll be plotting these variables against eachother. sns.jointplot() lets us create a plot with four components which can help us diagnose potential heteroscedasticity:

- The main plot is a scatterplot between hourly wages on the y axis, and years of schooling on the x axis.

- A regression line overlaid on this plot lets us see the relationship between our model and the underlying data

- A histogram to the right of the plot shows the distribution of the hourly wages variable, which is heavily skewed.

- A histogram above the plot shows the distribution of the years of schooling variable, which has an almost bimodal form.

sns.jointplot(data=reg_df, # plot a scatterplot with a regression line and two histograms

x='sch', # set the x axis to be the years of schooling

y='realhrwage', # set the y axis to be the hourly wage

kind="reg", # set the kind of plot to be a regression plot

scatter_kws=dict(alpha=0.1), # set the transparency of the points to be 0.1 (10%)

line_kws=dict(color='red'), # set the color of the regression line to red

height=10) # set the height of the plot to be 10 inches

plt.xlabel('Years of Schooling') # add a label to the x axis

plt.ylabel('Hourly Wage') # add a label to the y axisText(53.625, 0.5, 'Hourly Wage')

The plot above is cause for concern. From 0 to 5 years of schooling the model has underestimated hourly wages for every single observation. Conversely, at the far right tip of the regression line, we can see that the model overestimates income for many individuals with 18 years of schooling. This gives us reason to suspect that there may be asymmetry in the residuals of our model (heteroscedasticity). We’re going to fix this in the Exension section below. But for now, let’s proceed.

C. Multicollinearity

Multicollinearity emerges when two or more independent variables which are highly correlated are included in a model. A key goal of regression analysis is to isolate the relationship between each independent variable and the dependent variable. The interpretation of a regression coefficient is that it represents the mean change in the dependent variable for each 1 unit change in an independent variable when you hold all of the other independent variables constant.

The idea is that you can change the value of one independent variable and not the others. However, when independent variables are correlated, it indicates that changes in one variable are associated with shifts in another variable. The stronger the correlation, the more difficult it is to change one variable without changing another. See this blog post for a thorough explanation.

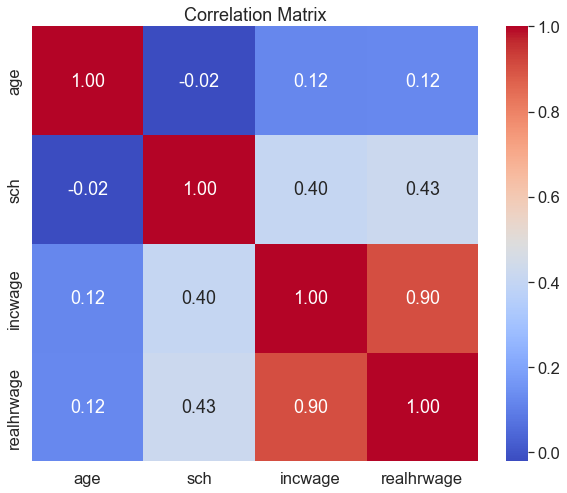

One way of visually exporing multicollinearity is through a correlation matrix:

sns.heatmap(reg_df[['incwage','realhrwage','age','sch']].corr(), # plot a correlation matrix

annot=True, # show the correlation values on the plot

fmt=".2f", # set the format of the correlation values to be two decimal places

cmap='coolwarm') # set the color palette to be coolwarm (blue for negative correlations, red for positive correlations)

plt.title('Correlation Matrix') # add a titleText(0.5, 1.0, 'Correlation Matrix')

This matrix has each of the continuous variables in reg_df on both axes. Each cell denotes the correlation between the corresponding variables. Naturally, on the diagonal we have a series of perfect correlations (1.00), as each variable is perfectly correlated with itself. incwage (annual salary) and realhrwage (hourly wage) are highly correlated with each other, which makes a lot of sense. This isn’t a concern for multicollinearity, though, since realhrwage will be our dependent variable. This type of correlation matrix is also a good way of conducting exploratory data analysis– we can already see that the next-highest set of correlations is between years of schooling and both hourly wages and annual salary.

Though a very high correlagtion coefficient between independent variables is a cause for concern, the formal way of dealing with muticollinearity is through the use of the Variance Inflation Factor (VIF). VIF is the ratio of the variance in a model with multiple predictors by the variance of a model with a single predictor:

\[\large VIF_j=\frac{1}{1-R_{j}^{2}}\]

VIFs start at 1 and have no upper limit. A value of 1 indicates that there is no correlation between this independent variable and any others. VIFs between 1 and 5 suggest that there is a moderate correlation, but it is not severe enough to warrant corrective measures. VIFs greater than 5 represent critical levels of multicollinearity where the coefficients are poorly estimated, and the p-values are questionable. More explanation of the theory can be found here.

Below is a function that calculates VIF for each independent variable in a dataframe, and drops them if they exceed a threshold (set to 5).

# calculating VIF

# This function is amended from: https://stackoverflow.com/a/51329496/4667568

from statsmodels.stats.outliers_influence import variance_inflation_factor

from statsmodels.tools.tools import add_constant

def drop_column_using_vif_(df, list_var_not_to_remove=None, thresh=5):

'''

Calculates VIF each feature in a pandas dataframe, and repeatedly drop the columns with the highest VIF

A constant must be added to variance_inflation_factor or the results will be incorrect

:param df: the pandas dataframe containing only the predictor features, not the response variable

:param list_var_not_to_remove: the list of variables that should not be removed even though it has a high VIF. For example, dummy (or indicator) variables represent a categorical variable with three or more categories.

:param thresh: the max VIF value before the feature is removed from the dataframe

:return: dataframe with multicollinear features removed

'''

while True:

# adding a constatnt item to the data

df_with_const = add_constant(df)

vif_df = pd.Series([variance_inflation_factor(df_with_const.values, i)

for i in range(df_with_const.shape[1])], name= "VIF",

index=df_with_const.columns).to_frame()

# drop the const as const should not be removed

vif_df = vif_df.drop('const')

# drop the variables that should not be removed

if list_var_not_to_remove is not None:

vif_df = vif_df.drop(list_var_not_to_remove)

print('Max VIF:', vif_df.VIF.max())

# if the largest VIF is above the thresh, remove a variable with the largest VIF

if vif_df.VIF.max() > thresh:

# If there are multiple variables with the maximum VIF, choose the first one

index_to_drop = vif_df.index[vif_df.VIF == vif_df.VIF.max()].tolist()[0]

print('Dropping: {}'.format(index_to_drop))

df = df.drop(columns = index_to_drop)

else:

# No VIF is above threshold. Exit the loop

break

return dfNow we can implement this on our dataset:

ind_vars=['sex','age','sch', 'union','race']

vif = drop_column_using_vif_(reg_df[ind_vars], thresh=5)

print("The columns remaining after VIF selection are:")

print(vif.columns)Max VIF: 1.0471509029112354

The columns remaining after VIF selection are:

Index(['sex', 'age', 'sch', 'union', 'race'], dtype='object')The maximum VIF value encountered was 1.04– well within the acceptable range. Accordingly, the function hasn’t dropped any of the independent variables in our dataset.

Having explored our data through visualizations and summary statistics, and checked the assumptions of linear regression, we’re now ready to begin building a model.

4. Regression

Remember, the Ordinary Least Squares (OLS) regression seeks to find a straight line that best describes the relationship between two variables:

\[y= \beta_0 + \beta_1x+\epsilon \]

In our case, we’re trying to predict hourly income– this is our dependent variable, and there can be only one per regression. The variable we’re using to predict hourly income is years of schooling, which is our independent variable. We can have multiple of these per regression. As such, the regression equation in our scenario looks like this:

\[Hourly\ Income= \beta_0 + \beta_1 \times Years\ of\ Schooling +\epsilon \]

Because the regression model will estimate the parameters \(\beta_0, \beta_1\) and \(\epsilon\), we just need to supply python with \(x\) and \(y\); We can do so by passing realhrwage ~ sch to the ols() function from statsmodels. This will run a regression of the form specified above, which we will store in an variable called model. We can get the output from this model using model.summary():

from statsmodels.formula.api import ols

from statsmodels.iolib.summary2 import summary_col

model= ols('realhrwage ~ sch', data=reg_df).fit() # fit the model

print(model.summary()) # print the summary OLS Regression Results

==============================================================================

Dep. Variable: realhrwage R-squared: 0.181

Model: OLS Adj. R-squared: 0.181

Method: Least Squares F-statistic: 1.164e+04

Date: Fri, 01 Dec 2023 Prob (F-statistic): 0.00

Time: 09:05:19 Log-Likelihood: -2.0503e+05

No. Observations: 52750 AIC: 4.101e+05

Df Residuals: 52748 BIC: 4.101e+05

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -6.6246 0.266 -24.858 0.000 -7.147 -6.102

sch 2.0327 0.019 107.887 0.000 1.996 2.070

==============================================================================

Omnibus: 10230.138 Durbin-Watson: 1.900

Prob(Omnibus): 0.000 Jarque-Bera (JB): 19817.137

Skew: 1.187 Prob(JB): 0.00

Kurtosis: 4.838 Cond. No. 73.7

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.There’s a lot going on in the regression output above. If you want a more detailed explanation of what each part means, check out this blog post. In practice, we only need to focus on a couple parts of this output:

R-squared: This value tells the proportion of the variation in our dependent variable (realhrwage) that is explained by the model we fit. In this case we can interpret it as follows:- 18.1% of the variation in hourly wages can be explained by this regresion model

coef: These are our \(\beta\) estimates; it is the slope of the regression line that describes the relationship between a given independent variable (sch) and the dependent variable (realhrwage). There are two coefficients listed under thissch: This is \(\beta_1\), the slope coefficient on the years of schooling variable. It tells us the change in \(y\) that results from a 1-unit increase in \(x\). In robotic terms, we can interpret it as follows:- A 1 unit increase in

schleads to a 2.0327 increase inrealhrwage. But we are not robots, and both of these variables are in units that we can interpret in plain english. Here’s a more natural interpretation: - On average, every additional year of schooling is associated with a $2.03 increase in hourly wages.

- A 1 unit increase in

Intercept: This is \(\beta_0\). It tells us the value of \(y\) when all of the independent variables in the model are held at 0. In this case, it can be interpreted as- According to our model, a person with 0 years of schooling is predicted to earn -$6.62 per hour

- Naturally, this is a nonsensical prediction. There are no jobs that pay negative wages. We’ll examine why this is happening in the next section, when we look into the assumptions of linear regression.

P>|t|: this is known as the “p-value”, and is the main measure of statistical significance. A p-value denotes the probability of obtaining a result at least as extreme as the one observed, assuming that the null hypothesis is true. In the case of a regression, the null hypothesis is that there is no relationship between our variables– increasing \(x\) has no effect on \(y\). In other words, that the regression line is flat: \(\beta_1=0\) . A p-value of 0.05 means that the coefficient is statistically significant at the 5% level. In our case, the p-value is 0.000 (note: this doesn’t mean it’s equal to zero, just very very small), and we can therefore reject the null hypothesis that \(\beta_1=0\) at the 1% confidence level. However, this isn’t the end of the story– remember our weird negative intercept, and the fact that our model explains less than 20% of the variation in hourly wages (\(R^2=0.181\)). For a good overview of what exactly a p-value is, and why we should be cautious when interpreting them, see this journal article.

Categorical Variables

The results of our first regression seem to show that the more education a person has, the higher their hourly wage. This makes intuitive sense, but it’s probably not the whole picture. We may also suspect that older people earn more, since they have more experience and are more senior. We’ve also seen i previous classes that there are significant disparities in income. Considering we have data on all these variables, we can set up the following model:

\[Hourly\ Income= \beta_0 + \beta_1 \times Years\ of\ Schooling + \beta_2 \times Age + \beta_3 \times Sex +\epsilon \]

When we convert this equation into the python equivalent, it will look like this:

realhrwage ~ sch + age + C(sex)

Notice that for the sex variable is put within C(). This is how we indicate that the variable in question is categorical, and that it should be treated differently. Unlike a continuous variable, we’re not interested in the change in \(y\) that results from a 1 unit increase in \(x\), since our units have no meaningful order. Instead, we’ll have to pick one of the categories (called a base category/reference category), and compare each of the other categories in that variable against this one. You can specify the base category explicitly (for example realhrwage ~ sch + age + C(sex, Treatment(reference=2)) makes women the base category), or python will pick one for you. As such, for a categorical variable with \(n\) categories, we get \(n-1\) coefficeints which denote the change in \(y\) associated with membership of a given category compared to the base category. For example, if we have a categorical variable with three levels \(a, b, c\) where \(a\) is the base category, we would get two coefficients: \(\beta_1 b\) and \(\beta_2 c\). Then we would interpret the resulting coefficient as

- “Compared to category \(a\), membership of category \(b\) is associated with a \(\beta_1\) change in \(y\).”

- “Compared to category \(a\), membership of category \(c\) is associated with a \(\beta_2\) change in \(y\).”

Let’s see what this looks like in our regression output:

model = ols('realhrwage ~ sch + age + C(sex)', data=reg_df).fit()

print(model.summary()) OLS Regression Results

==============================================================================

Dep. Variable: realhrwage R-squared: 0.239

Model: OLS Adj. R-squared: 0.239

Method: Least Squares F-statistic: 5514.

Date: Fri, 01 Dec 2023 Prob (F-statistic): 0.00

Time: 09:05:19 Log-Likelihood: -2.0310e+05

No. Observations: 52750 AIC: 4.062e+05

Df Residuals: 52746 BIC: 4.062e+05

Df Model: 3

Covariance Type: nonrobust

===============================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------

Intercept -12.6722 0.330 -38.392 0.000 -13.319 -12.025

C(sex)[T.2] -5.2692 0.099 -52.967 0.000 -5.464 -5.074

sch 2.1343 0.018 116.995 0.000 2.098 2.170

age 0.1695 0.005 36.164 0.000 0.160 0.179

==============================================================================

Omnibus: 9831.824 Durbin-Watson: 1.995

Prob(Omnibus): 0.000 Jarque-Bera (JB): 19481.335

Skew: 1.131 Prob(JB): 0.00

Kurtosis: 4.935 Cond. No. 308.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.We now have multiple coefficients in our regression model. As before, the Intercept typically isn’t very meaningful here — it would represent the predicted hourly wage for someone who is male, has 0 years of schooling, is 0 years old, and falls in all the baseline categories (e.g., the base race, base state, and base occupation). That’s not a realistic person, but it still provides a useful baseline for the model.

The key coefficients can be interpreted as follows:

C(sex)[T.2]: On average, women earn $5.2 less per hour than otherwise similar men.

Here,[T.2]refers to category 2 of the sex variable — women — while men (category 1) are the reference group. This is why you don’t see a coefficient forC(sex)[T.1]: the base category is absorbed into the Intercept.sch: Every additional year of schooling is associated with a $2.13 increase in hourly income.age: Every additional year of age is associated with a $0.16 increase in hourly income.

What does it mean to “control for” age and sex?

When we “control” for a variable in regression, we include it in the model so its influence on wages is accounted for. These factors matter:

- Age — older workers tend to earn more due to experience

- Sex — different demographic groups may face different wage structures

If we left these out, the coefficient on schooling might pick up their effects — leading to omitted variable bias.

By including these controls, we are comparing individuals who are similar in age and gender — but differ in schooling.

Interpretation of the schooling coefficient (with controls)

The coefficient on schooling tells us how wages are expected to change with one additional year of schooling, holding age, sex, state, race, and occupation constant.

This allows us to isolate the relationship between education and earnings, independent of the other factors that also influence wages.

Exercise

- Estimate a regression of the following form and store the results in a variable called model1:

\[Hourly\ Income= \beta_0 + \beta_1 \times Years\ of\ Schooling + \beta_2 \times Age + \beta_3 \times Sex + \beta_4 \times Union\ Membership + \beta_5 \times Race +\epsilon \]

- Intepret each of the coefficients appropriately. Make note of the statistical significance of each result, and comment on the overall fit of the model.

Creating a Regression Table

Now that we’ve got a good sense of how regressions work and how to interpret them, we need to communicate these results properly. Many of you have probably read journal articles in which regression results are reported, but I doubt you’ve ever seen the output of model.summary() copied and pasted in the text of an article. Instead, these results are reported following a fairly standardized convention: a regression table. It picks out the components of the model summary that we’re interested in, and formats them in a consistent and easy-to-interpret way. Luckly, the statsmodels package has a function called summary_col that takes a fitted model and formats it for us automatically; we just need to tweak a few options.

In the example below, i’m going to run two regressions; one in which i filter the data to only include people from California, and another for people in Mississippi (the richest and poorest states, respectively), to see if the relationship between wages, sex, age, and schooling differ geographically. I’m then going to create a regression table in which each column is a different regression model, and row will contain the coefficient for a given independent variable with the standard error in parentheses underneath and the level of statistical significance (i.e., size of the p-value) denotes by stars such that: * p<0.05, ** p<0.01, *** p<0.001.

california = ols('realhrwage ~ sch + age + C(sex)', data=reg_df[reg_df['state']==6]).fit() # fit a model to california-- i'm filtering the data using the FIPS code for california, which is 6

mississippi = ols('realhrwage ~ sch + age + C(sex)', data=reg_df[reg_df['state']==28]).fit() # same thing for mississippi (FIPS code 28)

table=summary_col( # create a regression table

[california,mississippi], # pass the models to the summary_col function

stars=True, # add stars denoting the p-values of the coefficient to the table; * p<0.05, ** p<0.01, *** p<0.001

float_format='%0.3f', # set the decimal places to 3

model_names=['California','Mississippi'], # set the name of the model

info_dict = {"N":lambda x: "{0:d}".format(int(x.nobs))}) # add the number of observations to the table

print(table)

=====================================

California Mississippi

-------------------------------------

Intercept -12.136*** -10.111***

(1.030) (3.497)

C(sex)[T.2] -5.154*** -4.980***

(0.350) (0.924)

sch 2.096*** 1.850***

(0.053) (0.205)

age 0.217*** 0.115**

(0.017) (0.045)

R-squared 0.262 0.199

R-squared Adj. 0.262 0.193

N 5079 430

=====================================

Standard errors in parentheses.

* p<.1, ** p<.05, ***p<.01This layout lets us clearly explore our regresison results. This lets us clearly compare the coefficients of the same variable in different models. For example, we can see that men tend to earn $5.15 more per hour than women in California, but just $4.98 more per hour in Mississippi, and both of these results are statistically significant at the 1% level. This suggests that the wage gap is actually somewhat higher in California! Why might this be?

Exercise

\[ Hourly\ Income= \beta_0 + \beta_1 \times Years\ of\ Schooling + \beta_2 \times Age + \beta_3 \times Sex + \beta_4 \times Union\ Membership + \beta_5 \times Race +\epsilon \]

- Run five regressions, each of the form above (same as earlier):

- In the first model, run the regression on the full sample contained in

reg_df. In subsequent modles, restrict the sample to the following professions:- Production

- Farmers

- Bankers

- Doctors & Lawyers

- In the first model, run the regression on the full sample contained in

- Create a regression table containing the results of each model in a separate column

- Interpret the coefficients on the union related variables

- How does union membership affect hourly wages across different sectors?

- How does the gender wage gap vary across sectors?

Extension

Though we’ve gotten some significant results and interesting insights from our modeling effort so far, we can further improve our model. In particular, we may want to revisit the way we’ve defined some of our variables, since we suspect that we may have some heteroscedasticity in our models, and have consequently been getting some weird results (e.g. negative hourly income).

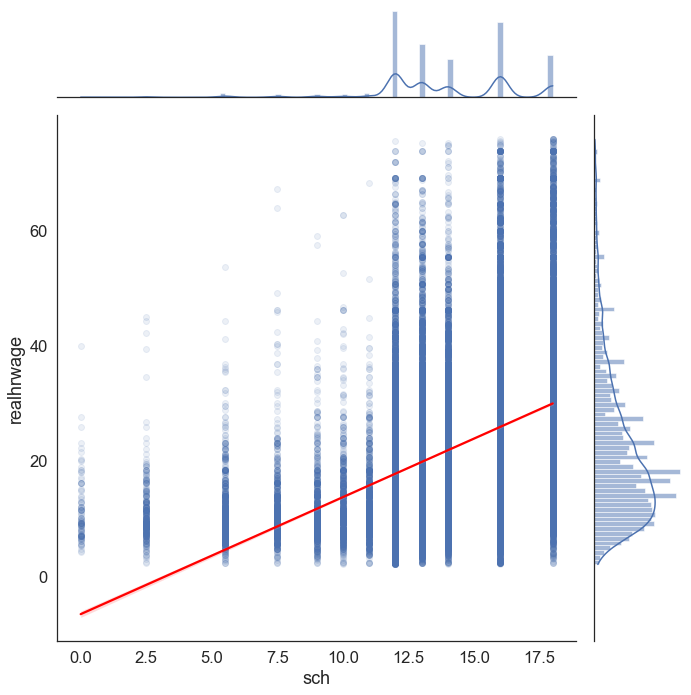

Hourly Wages

When checking the regression assumptions, we suspected that there may be some heteroscedasticity– i.e., that our model performs better in some regions of the \(x\) distribution compared to others; remember, it consistently underestimated hourly income for those with little/no schooling, as evidenced by the negative intercept and the regression scatterplot:

sns.jointplot(data=reg_df, x='sch', y='realhrwage', kind="reg", scatter_kws=dict(alpha=0.1), line_kws=dict(color='red'), height=10)

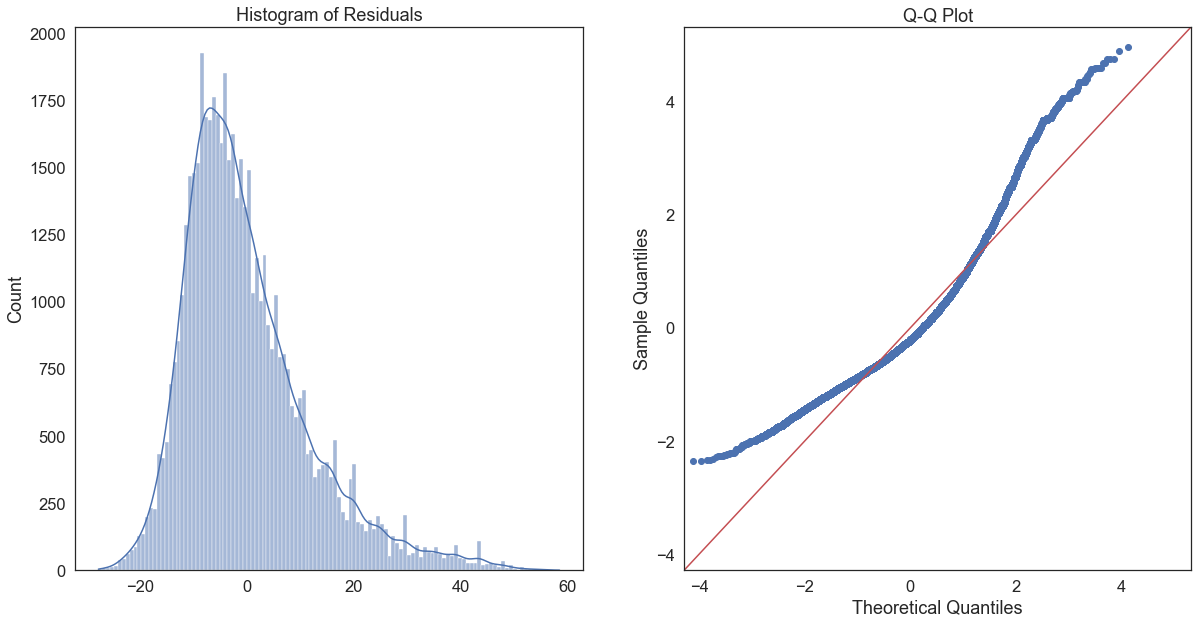

We can more thoroughly diagnose heteroscedasticity after having run our regression models, since we have access to the model’s residuals (the difference between the observed values and the predicted values). Remember, one of the assumptions of linear regression is that the residuals are normally distributed. A Quantile-Quantile Plot (Q-Q Plot) is a plot of the quantiles of a sample against the quantiles of a theoretical distribution. The quantiles are the values that divide the range of a probability distribution into continuous intervals with equal probabilities. Thus, we can use a Q-Q plot to compare the residuals of our model to a normal distribution as follows:

model = ols('realhrwage ~ sch', data=reg_df).fit() # fit a model

residuals = model.resid # get the residuals

# make the figure wider

plt.rcParams["figure.figsize"] = [20, 10]

f, axes = plt.subplots(1, 2)

sns.histplot(residuals, kde=True, ax=axes[0]) # plot the residuals

axes[0].set_title('Histogram of Residuals') # add a title

sm.qqplot(residuals, line='45', fit=True, ax=axes[1]) # plot the residuals

axes[1].set_title('Q-Q Plot') # add a title

plt.show() # show the plot

This Q-Q plot suggests that our residuals are not normally distributed, as very few of them are on the red line. This is probably due to the fact that the realhrwage variable is itself highly skewed.

Log transformations are often recommended for skewed data, such as monetary measures or certain biological and demographic measures. Log transforming data usually has the effect of spreading out clumps of data and bringing together spread-out data. So instead of:

\[Hourly\ Income= \beta_0 + \beta_1 \times Years\ of\ Schooling +\epsilon \]

we get:

\[\log{(Hourly\ Income)}= \beta_0 + \beta_1 \times Years\ of\ Schooling +\epsilon \]

In effect, this means changing our belief that there is a linear relationship between schooling and income (a constant increase in x leads to a constant increase in y across the whole range of x). Qualitatively, this means

reg_df['logwage']=np.log(reg_df['realhrwage'])

sns.jointplot(data=reg_df, x='sch', y='logwage', kind="reg", scatter_kws=dict(alpha=0.1), line_kws=dict(color='red'), height=10)

A few things are noticeably different in this plot. First, the histogram of logwage on the far right is a lot less skewed than the histogram of realhrwage. Consequently, the regression line seems to fit the data slightly better across the whole range of the data.

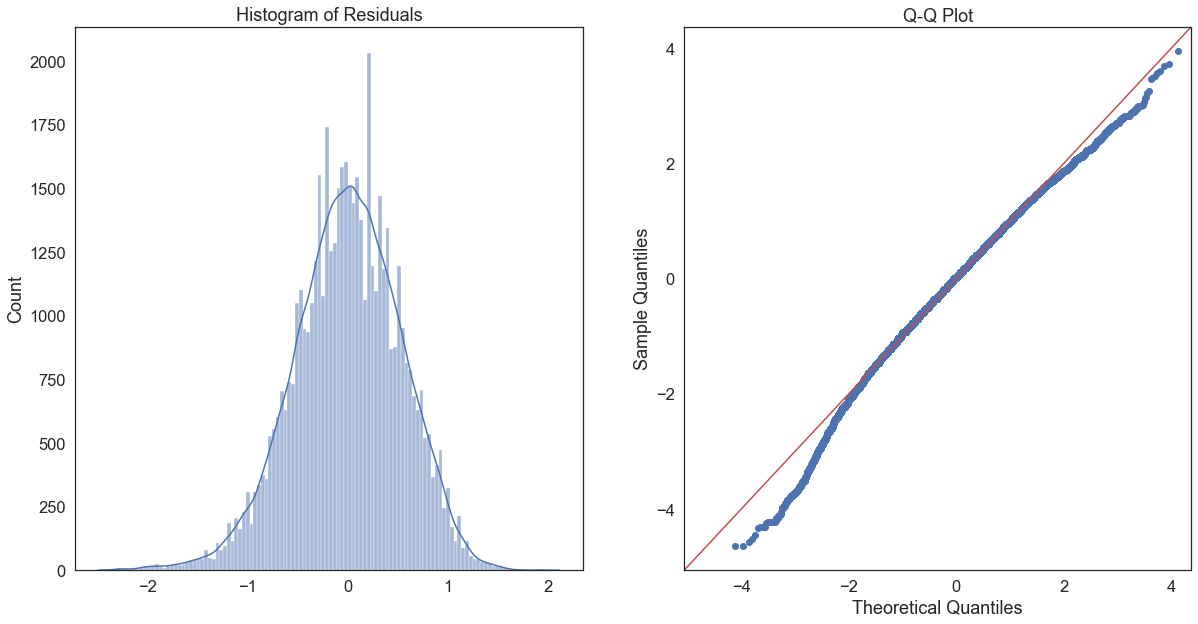

We can generate the same residual histogram and Q-Q plot as before, but using a model in which logwage is the dependent variable:

log_model = ols('logwage ~ sch', data=reg_df).fit() # fit a model

log_model_residuals = log_model.resid # get the residuals

# make the figure wider

plt.rcParams["figure.figsize"] = [20, 10]

f, axes = plt.subplots(1, 2)

sns.histplot(log_model_residuals, kde=True, ax=axes[0]) # plot the residuals

axes[0].set_title('Histogram of Residuals') # add a title

sm.qqplot(log_model_residuals, line='45', fit=True, ax=axes[1]) # plot the residuals

axes[1].set_title('Q-Q Plot') # add a title

plt.show() # show the plot

It’s not perfect, but it’s a lot better than the unlogged version; a large proportion of the residuals fall on the red line in the Q-Q plot, though they diverge at the tips. The histogram of residuals also seems to be less skewed, and more evenly distributed around 0.

Coefficient interpretation.

Only the dependent/response variable is log-transformed. Exponentiate the coefficient, subtract one from this number, and multiply by 100. This gives the percent increase (or decrease) in the response for every one-unit increase in the independent variable. Here’s a full guide to interpreting the coefficients on log-transformed variables.

First, let’s compare the unlogged and logged models:

table=summary_col( # create a regression table

[model,log_model], # pass the models to the summary_col function

stars=True, # add stars denoting the p-values of the coefficient to the table; * p<0.05, ** p<0.01, *** p<0.001

float_format='%0.3f', # set the decimal places to 3

model_names=['Unlogged','Logged'], # set the name of the model

info_dict = {"N":lambda x: "{0:d}".format(int(x.nobs))}) # add the number of observations to the table

print(table)

=================================

Unlogged Logged

---------------------------------

Intercept -6.625*** 1.573***

(0.266) (0.012)

sch 2.033*** 0.096***

(0.019) (0.001)

R-squared 0.181 0.191

R-squared Adj. 0.181 0.191

N 52750 52750

=================================

Standard errors in parentheses.

* p<.1, ** p<.05, ***p<.01Interestingly, we can see that we’ve also got a 1% increase in \(R^2\) just from logging the dependent variable. While the coefficient for schooling can be interpreted normally for the unlogged model (every additional year of schooling leads to a $2.03 increase in hourly wages), this is not the case for the logged model. We can interpret the coefficeint in the logged model as follows:

b1=log_model.params['sch'] # get the coefficient for sch

exp_b1=np.exp(b1) # exponentiate the coefficient

pct_change=(exp_b1-1)*100 # multiply by 100 to get the percentage change

print('For every additional year of schooling, log wages increase by {}%'.format(round(pct_change,2)))For every additional year of schooling, log wages increase by 10.04%Assessed Question

What is the percentage difference in log hourly wages for women compared to men, controlling for years of schooling, age, state, race, and occupation? Is this difference statistically significant at the 99% confidence level?